Putting $1000 in Micron stock at exactly the right moment turned into roughly $468,000. On November 21, 2008, MU shares crashed to an all-time intraday low of $1.59 during the depths of the global financial crisis, and investors who bought there and held through today’s price near $751 are sitting on returns north of 46,000%. That kind of Micron stock performance is rare. Right now, with the AI memory supercycle reshaping the entire semiconductor industry, the question is whether the Micron stock valuation gap and structural HBM demand can power another historic run for (NASDAQ: MU).

Also Read: MU Stock Is Up Today: Updated Price Target for 2027

Micron Stock Growth Potential, Valuation Gap and Performance Outlook

The Returns That Built MU’s Legend

Even investors who missed the 2008 bottom had a second shot. MU fell to $90.93 in spring 2025, during a broad market pullback that rattled a lot of conviction-heavy holders. From that entry alone, the stock surged to an all-time high of $818.67, also a gain of over 700% in under a year. So $1000 in Micron stock at that secondary low is, at the time of writing, worth around $8,200. The stock sits near $751 right now, with its entire 2026 HBM supply already spoken for and no meaningful new capacity arriving before 2028.

| Entry Point | Share Price | Approx. Return |

|---|---|---|

| All-time low — Nov 21, 2008 | $1.59 | >46,000% |

| Dot-com crash bottom — Jul 24, 1996 | $8.62 | >9,000% |

| Recent pullback — spring 2025 | $90.93 | >700% |

What Micron’s CEO Has Been Saying

Micron CEO Sanjay Mehrotra has not been subtle about the supply picture. On the Q1 FY2026 earnings call, he stated:

“The gap between the demand and supply for all of DRAM, including HBM, is really the highest that we have ever seen. We have completed agreements on price and volume for our entire calendar 2026 HBM supply.”

He also noted that Micron can currently meet only about 50% to 66% of demand from its key customers, and that tight conditions in both DRAM and NAND will stretch into 2027 or beyond. That is a pretty remarkable thing for a major chip company to say out loud. In fiscal Q2 FY2026, the company posted revenue of $23.86 billion, up 196% year over year, alongside record gross margins. On the earnings release, Mehrotra added:

“Micron set new records across revenue, gross margin, EPS, and free cash flow in fiscal Q2, driven by a strong demand environment, tight industry supply, and our strong execution. In the AI era, memory has become a strategic asset for our customers.”

The Valuation Gap Wall Street Has Not Fully Closed

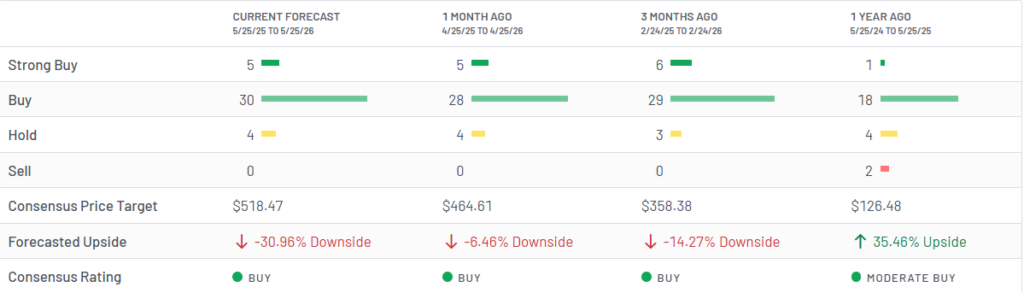

Based on 39 Wall Street analysts who have issued ratings in the past 12 months, MU carries a consensus “Buy” rating: 30 buy, 5 strong buy, 4 hold, and zero sell. The consensus 12-month price target sits at $518.47, which implies roughly 31% downside from $751. The Micron stock valuation gap between where the stock trades and where the average analyst puts it reflects a real split, with part of Wall Street still running old memory-cycle models and another part pricing in a structurally different AI demand environment. Deutsche Bank and DA Davidson both raised their targets to $1000, HSBC to $1100, while the most cautious target on the Street sits at $155.

Any Micron stock analysis built on forward earnings tells a different story. The stock trades at roughly 10x forward earnings, with EPS forecast to grow around 34% annually and projected return on equity near 49% over the next three years. Cloud memory and AI data center revenue now drive the dominant share of the business, and Micron stock growth potential ties directly to how long HBM demand stays ahead of supply.

Putting $1000 in Micron stock today is a different bet than it was in 2008 or even in spring 2025. The stock has already run hard and Micron stock performance over the past year has been extraordinary. But the supply math, with the demand-supply gap at the highest level Mehrotra says he has ever seen, is the kind of structural condition that has historically rewarded patience. Whether a third re-rating comes or not will probably depend on three things: HBM demand staying structurally ahead of supply, the company converting that tightness into expanding margins, and earnings continuing to outpace already-elevated expectations from here.