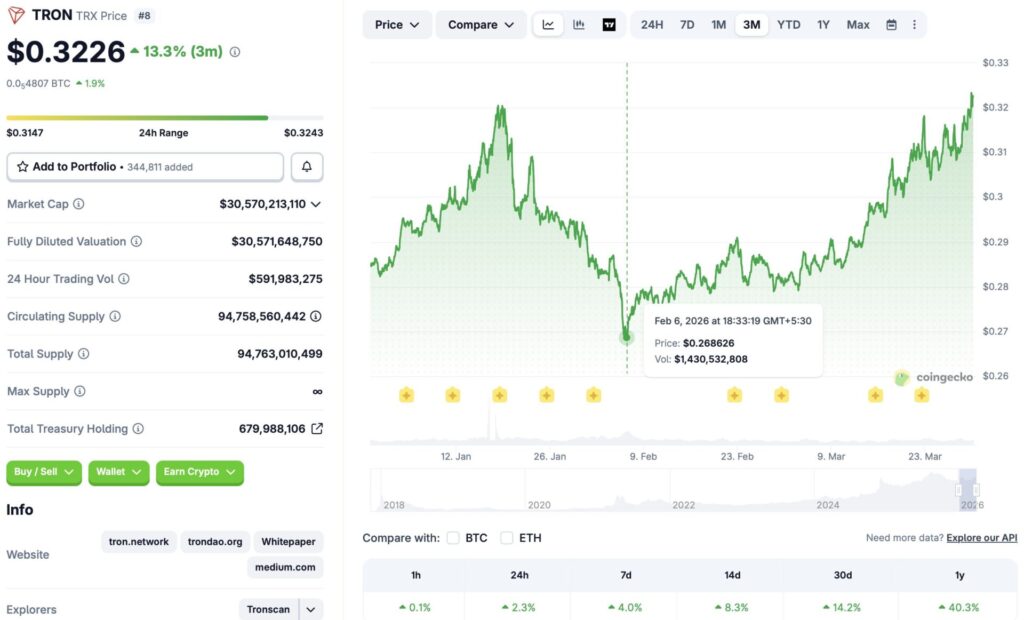

TRON (TRX) has displayed quite a performance over the last few weeks. While the market has faced a multiple swings since early February, TRX has maintained an upward trajectory. According to CoinGecko data, TRX’s price has surged 2.3% in the last 24 hours, 4% in the last week, 8.3% in the 14-day charts, 14.2% over the previous month, and 40.3% since late March 2025. Let’s discuss what’s behind TRON’s (TRX) price rally, and if the upswing can continue.

What’s Behind TRON’s Rally?

TRON (TRX) has seen a continued price appreciation since early February. The asset’s recent rally could be due to a number of factors. Firstly, the TRON DAO announced an expansion of its AI fund from $100 million to $1 billion. Given the surge in demand for AI-related services and the rise of AI-based stocks and cryptocurrencies, the announcement may have led to a massive surge in investor confidence.

Another reason for TRON’s (TRX) current price rally could due to Anchorage Digital announcing support for the TRON network. The partnership makes Anchorage Digital the first federally chartered bank to offer a partnership to TRON. The move may have pushed investor confidence even further.

TRON (TRX) has come a long way over the last few years. The network boasts high stablecoin liquidity, consistent transactions on the network, and real-world use cases in the form of payments and settlements.

Also Read: XRP Vs. Binance’s BNB: Which Is Better For Long-Term Growth?

Given that the developments around TRON (TRX) are central and not arbitrary, there is a chance that the price rally may be able to sustain itself. However, the larger crypto market seems to be facing another dip. Bitcoin (BTC) has fallen to the $67,000 price level after making another failed attempt at $72,000 last week. Given the bearish market environment, there is a possibility that investors will book profits and move their funds elsewhere. TRON’s (TRX) price could face a correction under such circumstances.