US Treasury borrowing is set to reach $578 billion in Q1 2026, the U.S. Department of the Treasury confirmed, assuming an end-of-March cash balance of $850 billion. At the same time, BRICS nations are cutting their exposure to American government debt. These are raising real questions about who is selling U.S. Treasuries, where the US Treasury yield goes from here, and what a U.S. debt-to-GDP ratio sitting above 120% actually means for Washington’s fiscal position.

Source: Watcher.Guru Based on

U.S. Department of the Treasury Data

Also Read: Prolonged Gulf Tensions Test India’s Trade, Energy, and BRICS Role

BRICS Treasury Sell-Off Raises Questions On U.S. Debt & Treasury Yield

$144.6 Billion Sold & US Treasury Borrowing Keeps Climbing

TIC data shows China cut its US Treasury holdings by $75.5 billion — around 10% — over the 12 months to December 2025. India trimmed its exposure by $36.2 billion, an 18% year-over-year drop, and Brazil shed $32.9 billion, roughly 16%. In November 2025 alone, China and India together offloaded $10.3 billion in US government debt. Who is selling U.S. Treasuries has gone from a vague concern to a well-documented pattern, and it sits right alongside US Treasury borrowing that just cleared a projected $578 billion for Q1 2026.

Bloomberg reported that Chinese regulators had been advising domestic financial institutions to limit their US Treasury exposure. They cited concerns around volatility and security. The report covered commercial banks rather than official reserve holdings, but markets took note regardless.

Paul Donovan, UBS Economist — stated:

“The idea that international investors may be less inclined to buy U.S. Treasuries in the future (without dumping existing holdings) is getting attention in markets.”

Chris Turner, ING Global Head of Markets — had this to say:

“Mainland China and Hong Kong together held $938 billion of U.S. Treasuries as of last November. Comments like these come at a vulnerable time for the dollar, when the dollar diversification theme is rife.”

Turner also described BRIC countries as “quietly leaving the Treasury market.”

US Treasury Yield Rises as U.S. Debt-to-GDP Approaches Historic Highs

The US Treasury yield on the 10-year note closed at 4.207% on March 11, up from 4.135% the session before. Iran’s strikes near the Strait of Hormuz pushed oil prices higher, and February’s CPI — core prices up 0.2% month-over-month — gave economists little reason to expect rate cuts anytime soon.

Some now put the Fed’s preferred core gauge at or above 3% for February, which also kept the US Treasury yield climbing through the week.

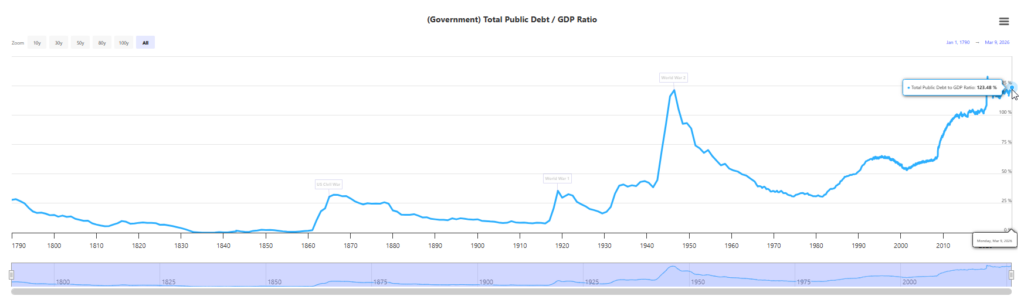

U.S. National Debt by Year Keeps Breaking Records

The U.S. debt-to-GDP ratio now stands at around 123.48%. That’s a level not seen since right after World War II, up from 79% before the pandemic and just 35% in 2008. Total public debt cleared $37 trillion, and the pace of US Treasury borrowing means interest payments now eat up roughly one-fifth of federal revenue.

Source: Long Term Trends

The CBO put government borrowing at around $308 billion in February 2026 alone, close to $50 billion a week over a five-month stretch. U.S. national debt by year data tells the same story. There’s a sharp, sustained climb with no reversal in the figures so far.

ING stated:

“Our baseline view for the dollar is a bearish one for the remainder of 2026. The concentration of risks in the US — from equity valuations to fiscal and political risks ahead of the midterm elections — means the risks remain on the downside for the greenback. We target 1.22 in EUR/USD by year-end.”

Also Read: BRICS Announce Thailand-Russia Business Forum

With US Treasury borrowing on track for another heavy quarter, the US Treasury yield holding above 4%, who is selling U.S. Treasuries showing up clearly in TIC data, and the U.S. debt-to-GDP ratio near post-war highs, the pressure on American finances right now looks broad. U.S. national debt by year figures keep climbing. Even more, nothing in the current pace of US Treasury borrowing suggests that changes soon.