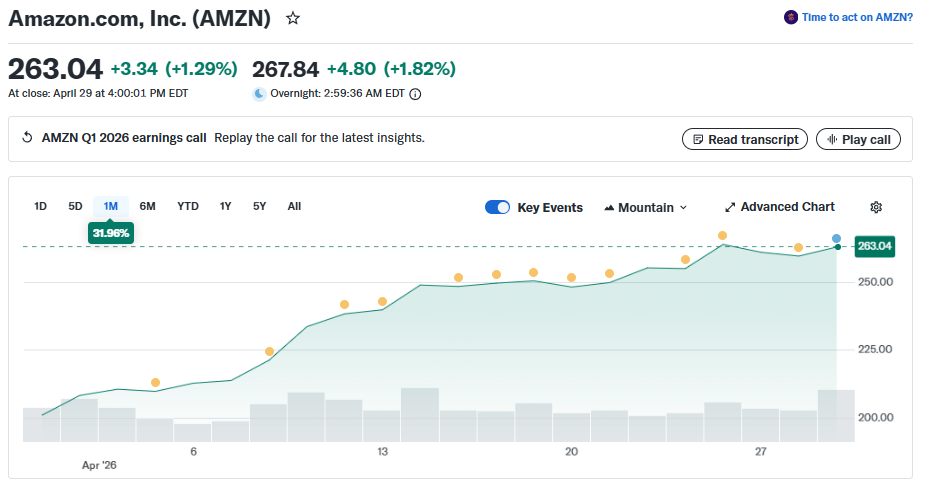

Amazon stock earnings for Q1 2026 came in sharply above Wall Street’s expectations. EPS hit $2.78 against a consensus estimate of just $1.64, and total revenue reached $181.52 billion, beating the $177.30 billion forecast. The Amazon earnings call on April 29 also delivered a strong Q2 outlook, with projected revenue of $194 to $199 billion. But the beat sits alongside a number that’s hard to ignore: Amazon cash flow on a trailing twelve-month basis dropped 95% year over year, falling to just $1.2 billion, as a $59.3 billion surge in AI infrastructure spending ate into returns. Amazon’s stock price gained more than 4% in after-hours trading, and right now the stock is up roughly 32% over the past month. Still, the question of whether $200 billion in planned 2026 capex will weigh on near-term returns is very much open.

Also Read: Google Stock Jumps on Earnings But UBS, Morgan Stanley See Bear Case

Amazon Earnings Call, Cash Flow Pressure, and Bearish Outlook Signals

AWS Powers the Beat

AWS grew 28% year over year to $37.59 billion, marking the fastest growth pace in 15 quarters and also the largest Q4-to-Q1 revenue increase in AWS history. The business now runs at a $150 billion annualized revenue rate, with AI services contributing over $15 billion of that figure in just three years. Advertising also held up well, rising 24% to $17.24 billion, ahead of the 21.2% growth Wall Street had forecast. Amazon stock earnings got a further lift from online stores, which grew 12% to $64.3 billion, also topping estimates.

Andy Jassy, CEO of Amazon, stated:

“We’re in the middle of some of the biggest inflections of our lifetime, we’re well positioned to lead, and I’m very optimistic about what’s ahead for our customers and Amazon.”

The Cash Flow Problem Wall Street Keeps Raising

Amazon cash flow for the trailing twelve months fell to $1.2 billion from $25.9 billion a year earlier, a 95% drop. Cash capex for Q1 alone came in at $43.2 billion, up from $25 billion in Q1 2025, with CFO Brian Olsavsky confirming on the Amazon earnings call that the spending tied primarily to AWS and generative AI investments. Amazon stock earnings may have cleared the bar on revenue and EPS, but the free cash flow line tells a different story, and that story is what’s driving the cautious tone from several Wall Street desks right now. Jassy pushed back on the capex concerns directly:

“We’re not investing approximately $200 billion in capex in 2026 on a hunch. Of the AWS capex we intend to spend in 2026, much of which will be installed in future years, we have high confidence this will be monetized well, as we already have customer commitments for a substantial portion of it, and that it will yield compelling operating margins and ROIC.”

Why the Bearish Signals Are Real

UBS analyst Stephen Ju reaffirmed a Buy on Amazon’s stock price and has a stock prediction target of $304, citing Amazon’s partnerships with Anthropic and OpenAI and a growing AWS backlog. He projects 38% AWS growth for 2026, well above the Street’s 26% consensus, and his 2027 operating income estimate runs roughly 39% above consensus too. But even Ju’s bullish projections come with an implicit acknowledgment of the core problem.

Also Read: Where Will Nvidia Stock Be in 10 Years? (NVDA)

AWS has to lay out cash for land, power, buildings, chips, and servers six to 24 months before billing customers, and right now that lag is very visible in the numbers. AWS growth for 2026 broadly lands in the 20 to 23% range across forecasts, fueled by surging AI demand, and yet Amazon cash flow keeps shrinking as that demand requires more and more upfront spending to serve. The Amazon stock bearish case does not require the business to fail. It just requires the $200 billion capex cycle to take longer to convert into free cash flow than the current Amazon stock price already prices in, and at the time of writing, that is a very reasonable concern for investors to hold.