Micron stock bull vs bear arguments have rarely been this far apart, and right now, with MU up more than 900% over the trailing 12 months, the debate is also getting louder. The stock briefly crossed the trillion-dollar market cap line on the back of AI-driven High-Bandwidth Memory demand, and yet there are also analysts calling it one of the most overvalued names in the market. Whether it is a buy or a sell, and also whether the current correction changes anything, depends on which side of the cycle clock you think we are on at the time of writing.

Also Read: Nvidia Stock Gets Strong Buy Call With a Price Target of $350 (NVDA)

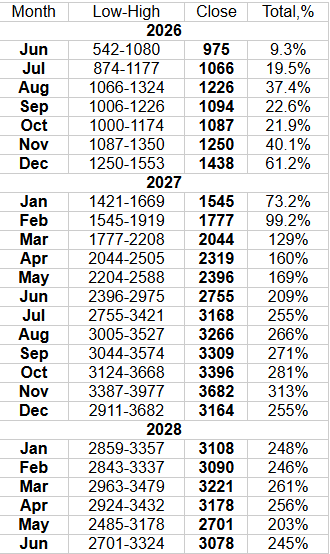

Micron Stock 2026 Prediction, Bull Case, Micron Stock Bullish Reviews & Micron Stock Bear Market

The Bull Case: HBM Locked Out, And Hyperscalers Still Spending

The Micron stock bull case rests on a supply shortage that has not let up. HBM supply sold out through 2026 under long-term contracts, and Goldman Sachs projected the deepest memory shortage on record extending into 2028. Fiscal Q1 2026 revenue came in at $13.64 billion, up 57% year-over-year, with non-GAAP EPS of $4.78 beating consensus estimates by more than 21%. Analyst targets have been climbing fast too: UBS sits at $1,625 and Susquehanna at $1,750. A Micron stock 2026 prediction built around those numbers assumes the AI infrastructure wave stays intact, and so far the hyperscalers have given no sign of pulling back on spending.

Rob Thummel, senior portfolio manager at Tortoise Capital, told MarketWatch:

“From a macro perspective, the AI industrial revolution continues. The spending still seems to be there, the AI applications are coming and you need infrastructure to support them.”

Adam Patti, CEO of ETF manager VistaShares, said:

“The reality is that chip stocks have had a massive run-up, but for good reason — the fundamentals are there. I think we’ll see some type of retrenchment, and then there’ll be continued upside based on the fundamentals and the fact that there’s so much capex being deployed.”

Also Read: Micron’s Two-Year Sellout Fueled a 918% Surge: Is MU Still a Buy?

The Bear Case: Valuation, Insider Selling, And A 2029 Revenue Cliff

The Micron stock bear market argument starts with valuation. Morningstar analyst William Kerwin, CFA, puts fair value at $455 per share, which at the time of writing means MU trades at more than twice that figure. A harsh 50% revenue downcycle sits in the forecast for 2029, as new semiconductor capacity floods the market.

Insider activity also points bearish: CEO Sanjay Mehrotra sold shares across 25 separate transactions in May 2026, in the $511 to $545 range. 24/7 Wall St. carries a sell rating at a $435.15 price target with 90% confidence, citing an implied P/E of 71 on a historically cyclical business. MU has already dropped more than 17% from its June 3 record close, and the broader XLK tech ETF entered official correction territory on June 10, down 10.9% from its peak. The Micron stock bull vs bear divide is no longer theoretical.

Should I Sell Micron? What Both Sides Agree On

Analysts on both sides of the Micron stock bull vs bear debate agree on one thing: the Q3 earnings call on June 24 is the real test. Bulls say a guidance beat confirms the $1,000-plus level as a durable re-rating. Bears say any softness in HBM pricing sends the stock sharply lower, given how much optimism has been priced in already. The Micron stock 2026 prediction also splits along those same lines, with the average analyst consensus target sitting near $717, well below where MU trades at the time of writing, even as the most aggressive Micron stock bullish reviews push targets past $1,500. Whether you sell, hold, or buy more, that earnings print is the number everyone is watching right now.