The MSFT stock 2026 forecast is getting a fresh look this week after Microsoft posted a record Q3 FY2026 earnings report that beat expectations across the board. Revenue came in at $82.9 billion, up 18% year over year, with GAAP diluted EPS of $4.27 and operating income of $38.4 billion, up 20%. Azure grew 40% in the quarter, and Microsoft’s commercial backlog hit $627 billion, up 99% year over year, a number that tells you a lot of future revenue is already locked in. Microsoft’s AI business also surpassed a $37 billion annual revenue run rate, up 123% year over year, and Copilot paid seats crossed 20 million, up 250% year over year.

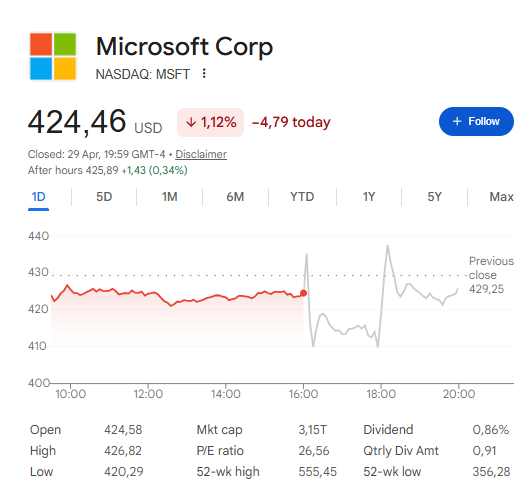

Even so, Microsoft shares are still down roughly 15% year-to-date as of late April 2026, after hitting a 52-week high of $555.45, and that gap between strong fundamentals and a weak stock price is exactly what analysts are trying to make sense of right now. Whether Microsoft stock will recover, and how fast, remains the central question.

Also Read: 5-Star Analyst Warns on Microsoft Stock as Earnings Test Nears

MSFT Stock Outlook 2026: AI Spending, Azure Growth & Price Targets

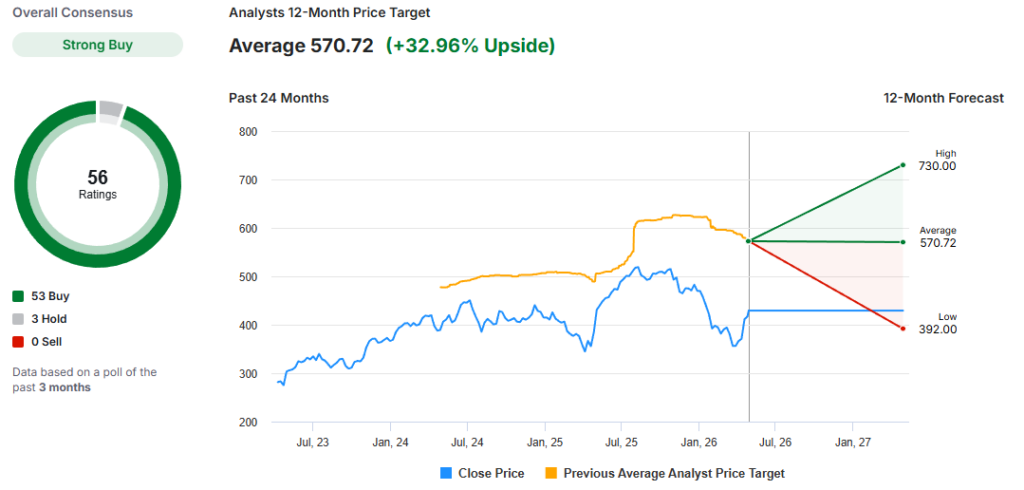

According to Investing.com data, 56 analysts currently hold a “Strong Buy” consensus on Microsoft, with an average 12-month price target sitting at $570.72. The high target is $730, and the most bearish projection sits at $392.

Sell Source: Investing

What the Bulls are Saying about the MSFT Stock 2026 Forecast

Wedbush analyst Dan Ives reiterated an “outperform” rating with a $625 MSFT price target for 2026. He stated:

“Wall Street is underestimating the growth prospects for Microsoft’s Azure cloud” and that AI monetization will significantly boost profits in 2026-2027.

Morgan Stanley lifted its own target to $650, calling Microsoft a top pick and pointing to the company’s growing role in enterprise AI adoption. Bernstein also raised its target to $641, noting the engine of growth is strong and getting stronger, with Azure growth exceeding expectations as a key driver.

The Q3 FY2026 numbers back up that optimism. Microsoft Cloud revenue hit $54.5 billion, up 29% year over year, and the Intelligent Cloud segment brought in $34.7 billion, up 30%. Azure grew 40% and came in ahead of expectations. CEO Satya Nadella stated on the earnings call:

“It was a record third quarter, powered by the continued strength of the Microsoft Cloud, which delivered $54 billion in revenue, up 29% year over year. Our AI business surpassed $37 billion ARR, up 123%.”

CFO Amy Hood also stated:

“We delivered results that exceeded expectations across revenue, operating income, and earnings per share, driven by strong demand and execution.”

A lot of the MSFT stock 2026 forecast debate now centers on whether Azure growth and AI spending can keep accelerating through the back half of the year. Hood guided for Q4 Azure growth of 39% to 40% in constant currency, with modest acceleration expected in the second half of calendar 2026.

The Bear Case Weighing on the MSFT Stock 2026 Forecast

Capex hit $31.9 billion in Q3 FY2026 alone, and Microsoft guided for over $40 billion in Q4, with total calendar year 2026 capex now projected at $190 billion, up 61% from 2025. That is the number bears keep coming back to, and it includes roughly $25 billion from higher component pricing. Free cash flow came in at just $15.8 billion in the quarter, reflecting the weight of those capital expenditures. Infrastructure costs are running well ahead of revenue growth right now, and that puts real pressure on margins in the near term.

The Copilot story is also more complicated than the headline seat number suggests. Analysts once projected M365 Copilot could generate $30 billion in annual revenue. Estimates put last year’s actual revenue from the product at just $1.4-$3.2 billion, drawn from a small subset of Microsoft 365’s 450 million commercial users. Many enterprises say the ROI simply does not justify the premium per-user pricing, and bears note the product is still early in proving it can drive revenue at scale.

On the OpenAI partnership, Microsoft revised its agreement this week. Hood confirmed the key terms on the earnings call:

“Having the revenue share exist through 2030, the predictability of that is a real positive for us, and, as Satya pointed out, the IP being royalty-free with the elimination of our rev share to them.”

Bears will note OpenAI is still expected to spend heavily through 2030 while revenues remain small relative to costs, which keeps the dependency risk alive even under the new structure.

Also Read: Citi Analyst Says Johnson & Johnson Stock To Reach $285, 27% Profit

Will Microsoft Stock Go Up? What the Data Suggests

The bull case for the MSFT stock 2026 forecast rests on Azure growth reaccelerating in the second half of the year as new capacity comes online. The $627 billion commercial backlog, up 99% year over year, gives bulls a concrete floor of contracted future revenue that is hard to argue with. Copilot paid seats at 20 million, up 250% year over year, and weekly engagement now at Outlook levels also suggest the monetization story is starting to move. Out of roughly 97 analysts covering the stock, the majority rate MSFT a Strong Buy or Buy, with an average price target in the $589-$592 range.

The stock also trades at around 21x-22x forward earnings right now, its cheapest valuation since 2023. Analysts at Benchmark called the recent pullback a long-term buying opportunity when they initiated coverage with a Buy rating. Whether the MSFT stock 2026 forecast plays out the way bulls expect will largely come down to how fast AI spending translates into measurable margin improvements and whether Azure growth continues to accelerate into H2. Microsoft stock going up from here looks more achievable after these Q3 numbers, but the $190 billion capex commitment and the pace of Copilot monetization at scale are still the two questions without clean answers yet.